Argos Fraud Shows The Retail ATO Problem Has Left The Browser

Leaked credentials, online accounts, and Click & Collect turn account takeover into a storefloor control failure.

Leaked credentials, online accounts, and Click & Collect turn account takeover into a store-floor control failure.

The Argos fraud spike is not just another reminder that people reuse passwords.

It is a reminder that retail identity controls now have a physical endpoint.

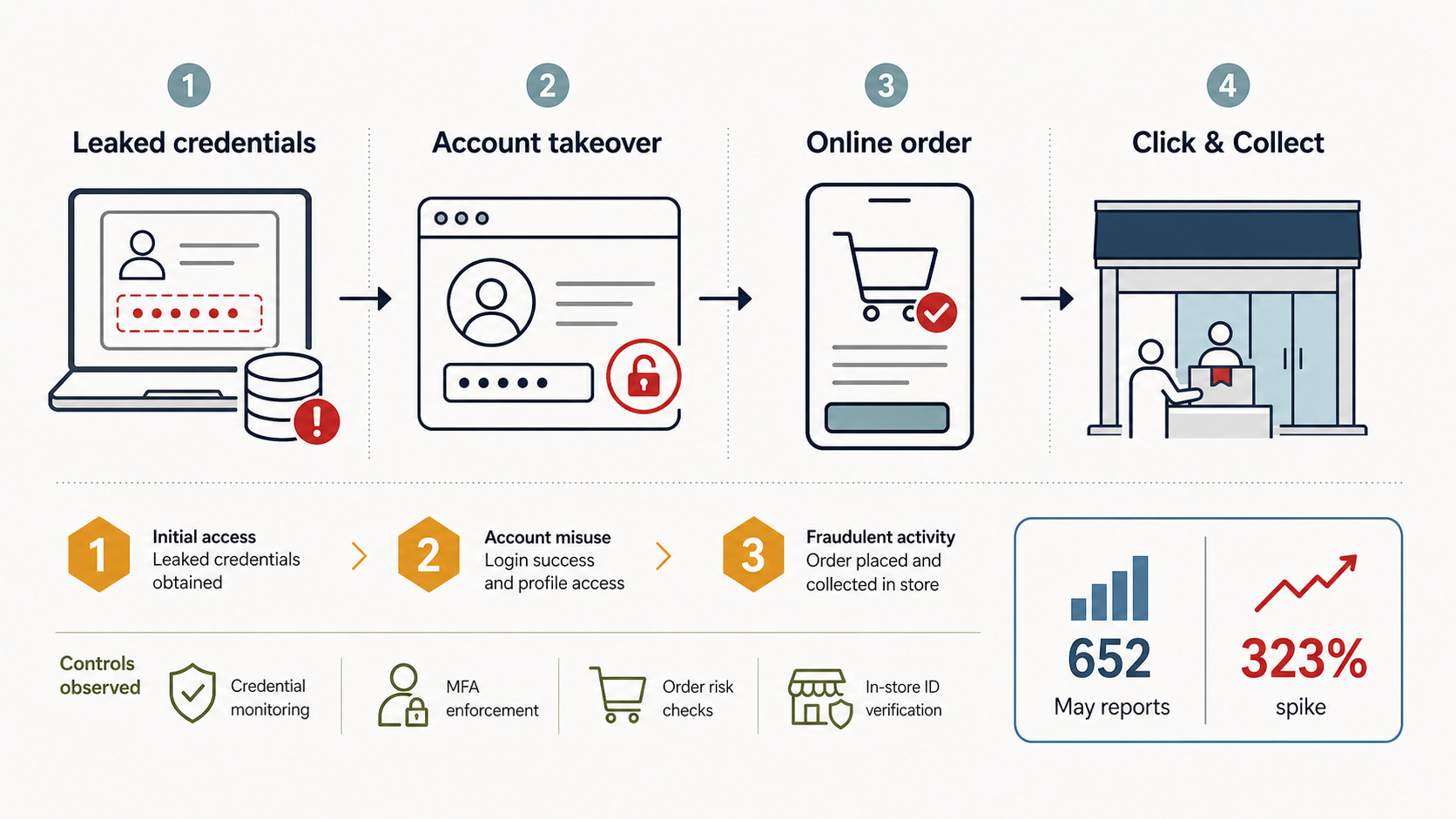

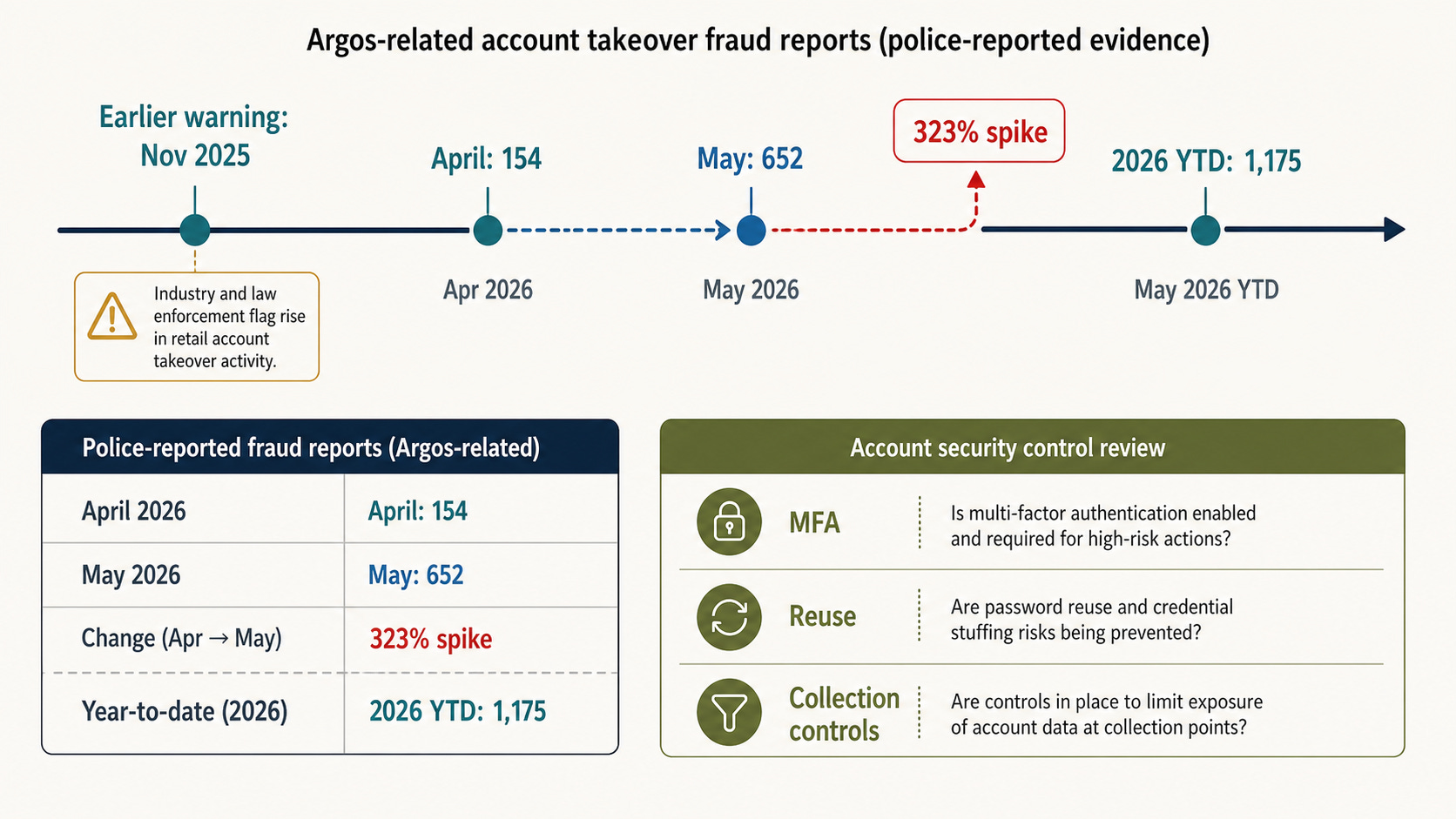

According to BushidoToken's write-up of UK police reporting, Report Fraud saw 652 reports mentioning Argos in May 2026, up from 154 in April. That is a reported 323% month-over-month spike in cases tied to a familiar fraud pattern: criminals gain access to customer retail accounts, place orders, and collect goods in person.

The useful lesson is not that Argos is uniquely exposed. The lesson is broader and more uncomfortable for retail risk teams: when online identity is weak, store operations inherit the fraud.

The Account Is The Pickup Ticket

The City of London Police warning cited by BushidoToken says criminals are using credentials leaked in historical data breaches to hijack Argos accounts. Once inside, they can place orders and retrieve goods through Click & Collect.

That makes the customer account more than a login.

It becomes the fraud actor's pickup ticket, purchase context, and legitimacy layer. A familiar account with order history can look less suspicious than a brand-new identity, especially if the transaction is routed through ordinary retail workflows.

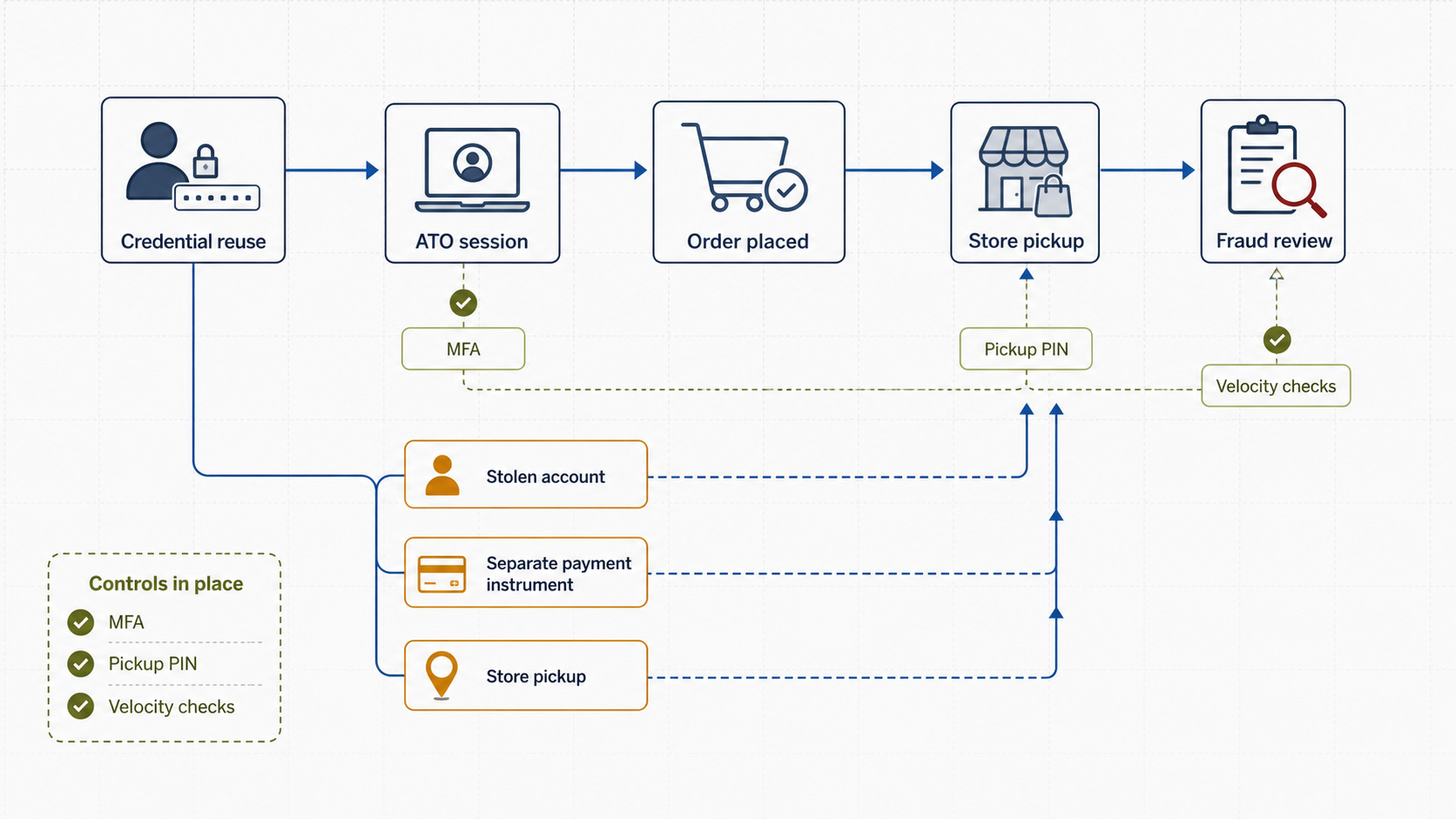

BushidoToken also notes that some fraudulent orders were reportedly paid for using payment details not connected to the account victim. That matters because it blends two signals that many teams still treat separately: compromised customer identity and separate payment fraud.

The result is a messy operational case. The victim may own the account. A different stolen payment instrument may fund the order. The goods may leave through a legitimate collection lane.

No single team owns that whole chain by default.

Convenience Became The Attack Surface

Click & Collect is designed to be fast. That is the product promise.

But speed changes the fraud window. If a criminal can move from account access to order placement to in-store collection before the real account holder notices an email or push notification, the control point has shifted from the website to the store counter.

That does not mean retailers should make collection painful for everyone. It means high-risk collection events need context.

An account that suddenly orders higher-value goods, changes delivery or collection behavior, uses a new device, or combines suspicious login patterns with separate payment signals should not be treated like a normal repeat purchase.

The practical question is simple: can the retail system tell store staff when a pickup requires stronger verification without turning every collection into a manual investigation?

The Numbers Point To A Control Gap

The police figures in the BushidoToken summary are sharp enough to treat as an operational warning.

May had 652 reports mentioning Argos. April had 154. Since the start of 2026, there were 1,175 reports mentioning the retailer, with May the highest month cited in the alert.

There was earlier public warning activity too. BushidoToken references a November 2025 East Midlands Cyber Resilience Centre warning about Argos and Currys accounts being compromised and unauthorized purchases being made. In some Currys cases, the report says Buy Now Pay Later options were used, creating finance-plan risk for account holders.

That earlier warning matters because it shows the pattern is not limited to one month or one retailer's queue. Retail accounts, saved identity context, payment workflows, finance options, and pickup operations are all converging into one fraud surface.

Breach Data Is Still Paying Dividends

This is where historical data breaches keep compounding.

Credential stuffing does not require a new breach at the targeted retailer. It relies on old username and password pairs, password reuse, and weak or optional step-up controls. Cloudflare describes credential stuffing as attackers using previously exposed login pairs against other services at scale.

For retail, that means yesterday's breach at an unrelated service can become today's account takeover queue.

MFA, passkeys, password managers, breached-password checks, and anomaly detection are not cosmetic account-security features. They are loss-prevention controls. They decide whether a stolen password becomes a completed collection.

The same applies to rate, source, and device context. If a proxy-heavy source IP is attempting logins across many accounts, or if successful sessions cluster around new devices and unusual purchase behavior, the fraud program needs that signal before goods are handed over.

The Store Counter Needs Risk Context

The least useful response would be to push the whole problem onto store staff.

Collection workers should not have to become fraud analysts. They need simple, reliable prompts backed by online identity telemetry: request ID, require a one-time pickup code, ask for stronger identity verification, or escalate the order before release.

That is where online and physical controls need to meet.

High-risk actions can trigger step-up authentication before the order is confirmed. High-value Click & Collect purchases can require a single-use PIN or QR code sent through a trusted channel. BNPL or finance-plan creation can require stronger identity proofing than a normal basket checkout. Collection events can inherit risk decisions already made online.

None of this needs exploit detail. It needs business-process discipline.

Treat Retail ATO As An End-To-End Workflow

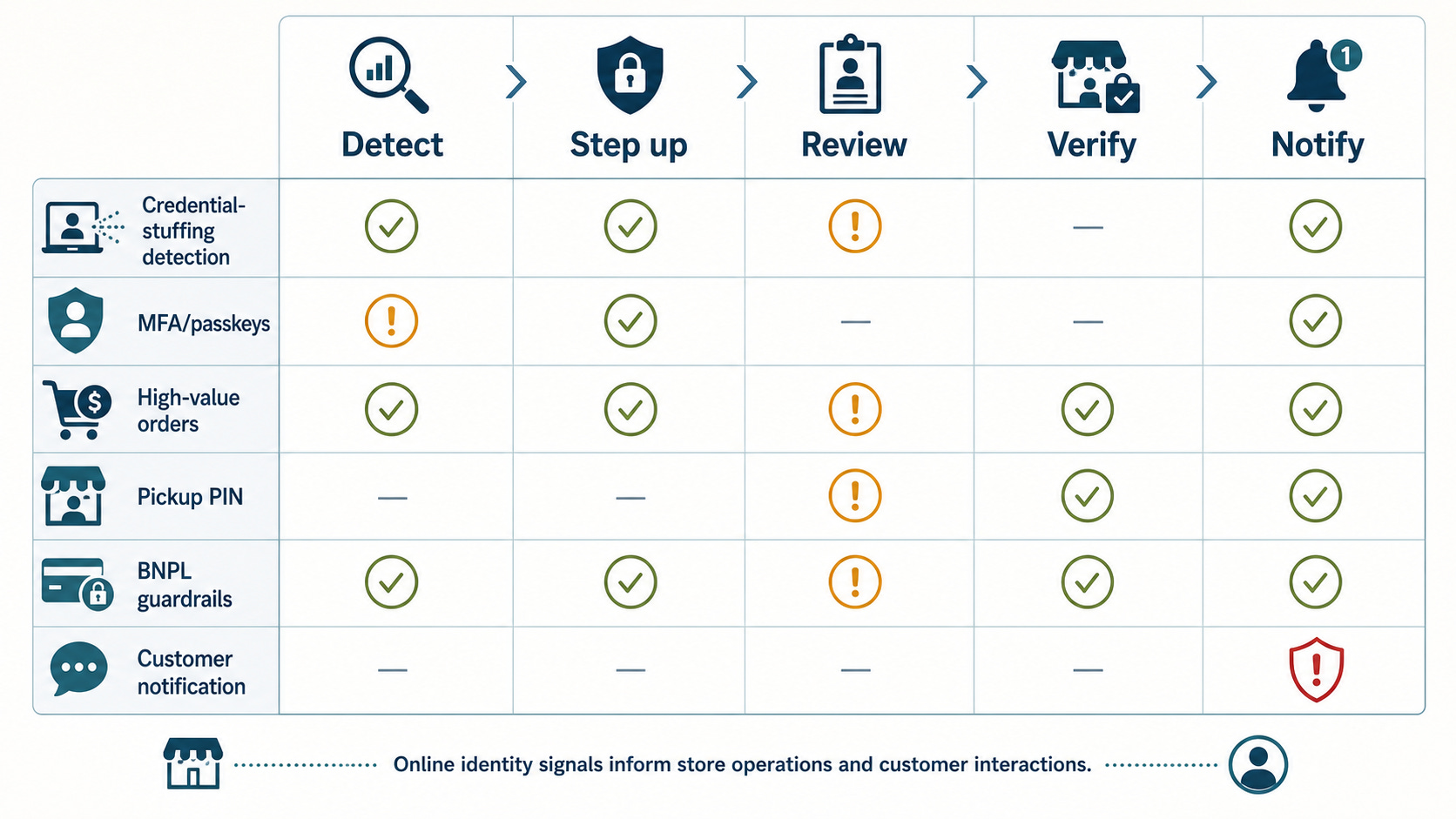

The useful control model is end-to-end.

Detect credential-stuffing patterns. Step up risky sessions. Review unusual orders before fulfillment. Verify the person collecting high-risk goods. Notify customers quickly when account behavior changes.

The order matters less than the handoff. A login risk signal that never reaches fulfillment is wasted. A store verification policy that has no idea which orders are risky becomes friction without precision. A fraud review that starts after goods leave the store is already late.

Retail account takeover is no longer contained inside the browser.

For defenders, that is the central point. Account security, fraud operations, payment risk, BNPL governance, and store collection processes are now part of the same incident surface. If they do not share signals, criminals can move through the gaps using the retailer's own convenience model as the path.